")

Table of Contents

FangXiaNuo/iStock via Getty Images

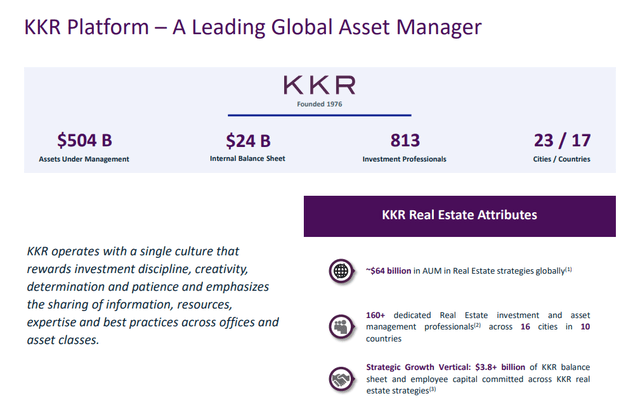

KKR Real Estate Finance Trust Inc. (NYSE:KREF) is one of the better known commercial mortgage REITs. The name is well known though as the sponsor (KKR), has been a favorite alternative asset manager.

KREF Presentation

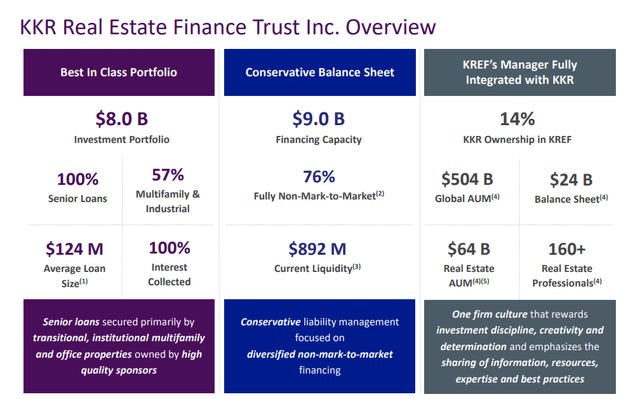

Further, there are aligned investor interests and KREF’s manager owns a low double digit stake.

KREF Presentation BXMT Q4-2022 Presentation

Investments

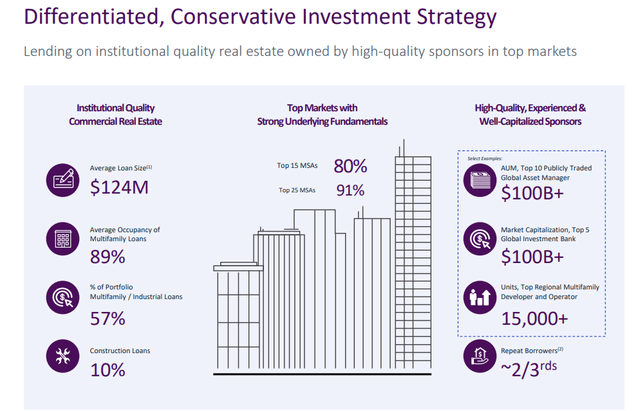

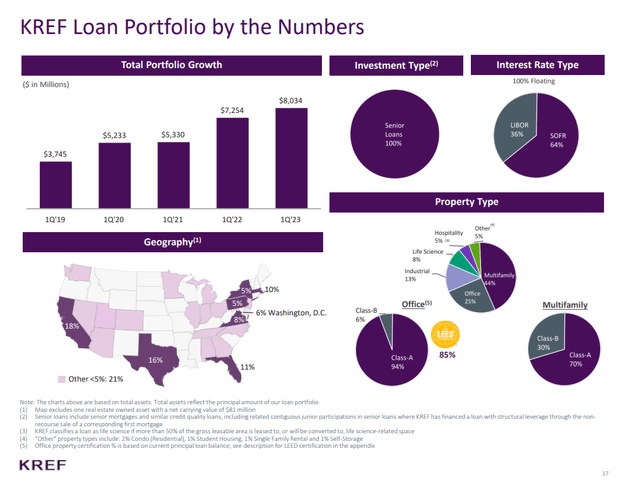

KREF focuses on medium sized loans with an average size near $125 million.

KREF Presentation

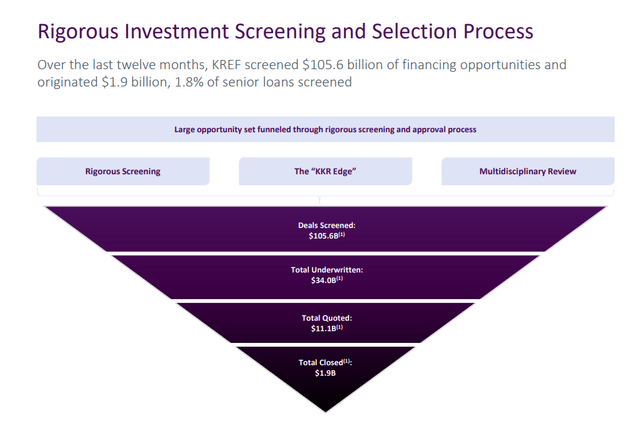

The firm screens a high amount of loans in relation to its approvals and the breadth and depth of KKR expertise certainly aids this process. Over the last year, less than 2% of screened loans were given a green light.

KREF Presentation

One thing to keep a watch on here is the exposure to the office sector. KREF has about one quarter of its loans tied here and we will add that the hospitality sector forms another 5% of the total. Multifamily, which would make for a more defensive asset formed 44% of the total. The combination of multifamily and industrial property loans is the highest amongst its peers. BXMT had about 32% in this area on last check vs 57% for KREF.

KREF Presentation

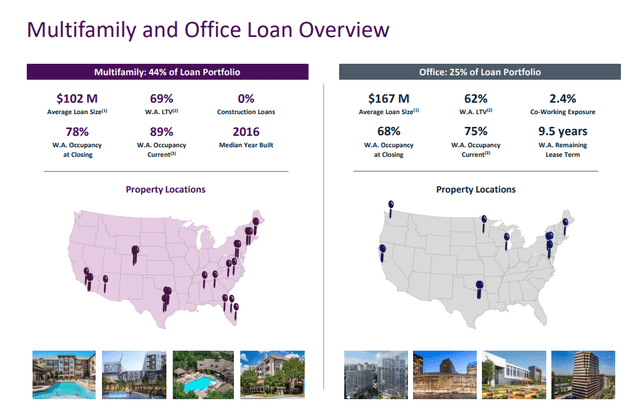

While the multifamily loans appear great, one must remember that these are not the traditional loans that banks make. The reason KREF is involved is because the asset in general is riskier and has a higher default risk. The same goes for the office side, except that everyone already knows the risks there.

KREF Presentation

Overall, KREF has a better than average portfolio from asset standpoint amongst its peers. This has to be weighed against the relatively rapid growth of the total portfolio size in the last 2 years. Obviously the more loans that were originated at a time of inflated property values, the bigger the risk to the company, despite supposedly low loan to value ratios.

Q1-2023

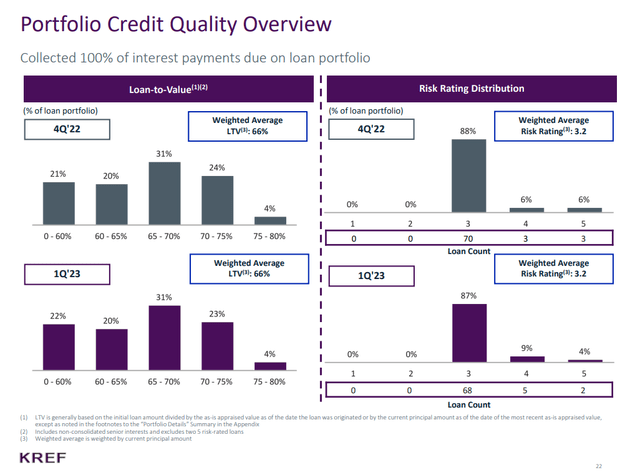

KREF’s credit quality looked ok at the end of Q1-2023 with only 13% of loans in the 4 and 5 risk categories. The weighted average risk rating was unchanged from last quarter.

KREF Presentation

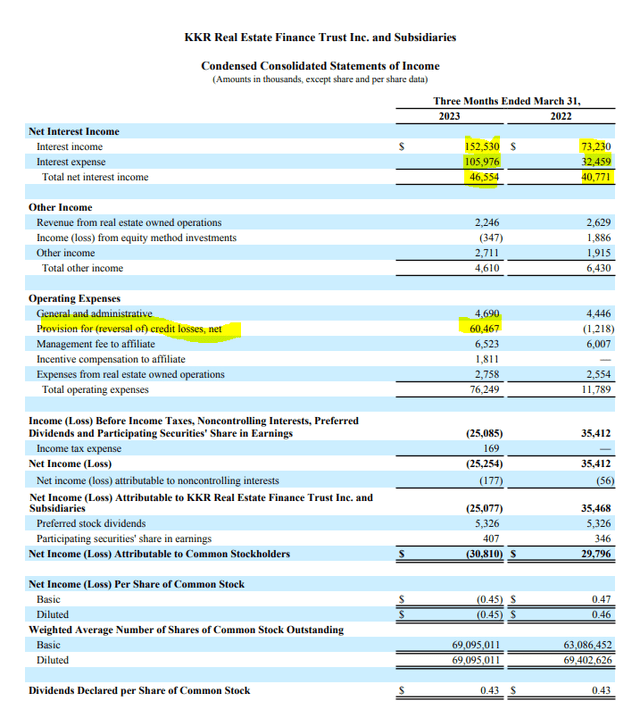

The income statement showed a rising net interest income picture but one that was marred by a massive provision for credit losses.

KREF Presentation

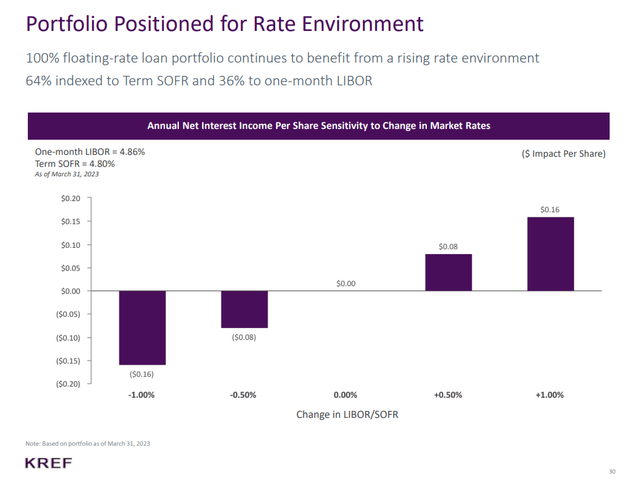

The bull contention will of course be that they have taken the write downs and the stock promises upside. This argument is supported further by KREF’s sensitivity to further rate hikes.

KREF Presentation

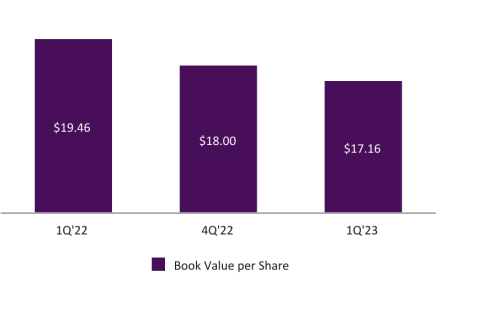

A final piece of the puzzle is that the current book value is still miles ahead of the stock price.

KREF Presentation

Should you bite?

Risks

Mortgage REITs run a high level of leverage and this level varies depending on the asset class. Agency mortgage REITs which dabble in mortgage backed securities tend to run the highest ratios as the underlying asset class is safe from a credit perspective. Commercial mortgage REITs run lower ratios in general. Here we see KREF with total assets to equity near 5.2X.

KREF Presentation

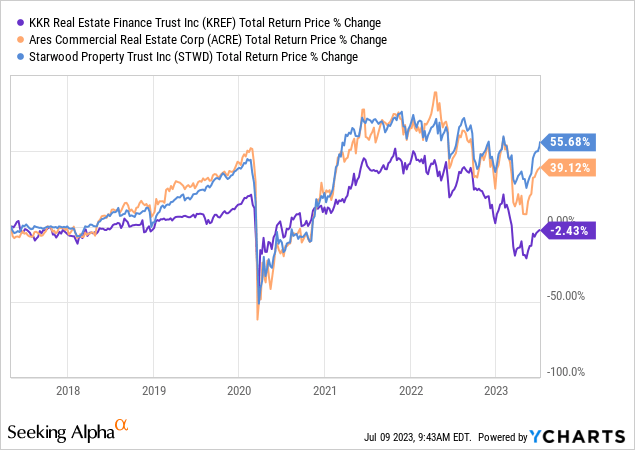

How high is that? Well let’s see Ares Commercial Real Estate Corporation (ACRE).

ACRE Presentation

The same ratio is at 3.4X. You can see just how much more risk is there in the KREF portfolio just from a leverage perspective. Of course there are those that take the same levels of risk.

We previously covered the largest player in this sector, Blackstone Mortgage Trust, Inc. (BXMT). BXMT was at 5.6X, even higher than KREF.

BXMT Presentation

Without getting into the rest, we can tell you that KREF is running leverage at the very high end of this sector and also at the high end of what we think is feasible for this portfolio. Yes, we are taking into account the better performing assets embedded here. In fact, Moody’s (MCO) looked at all the data and decided to drop them further into junk territory about a month back.

New York, June 09, 2023 — Moody’s Investors Service (Moody’s) has downgraded KREF Holdings X LLC’s senior secured credit rating to Ba3 from Ba2. Moody’s has also affirmed KKR Real Estate Finance Trust Inc.’s Ba3 corporate family rating (CFR). The outlook remains stable.

While the affirmation of the Ba3 long-term CFR resulted from Moody’s unchanged view of the company’s standalone assessment, the downgrade of the long-term senior secured rating to Ba3 from Ba2 reflects lower protection to senior creditors because of an increasing amount of senior debt relative to unsecured debt.

RATINGS RATIONALE

The downgrade of the long-term senior secured rating to Ba3 from Ba2 follows increased borrowing on secured lending facilities relative to unsecured obligations. The declining proportion of unsecured debt in the capital structure no longer provides as much protection to senior secured creditors.

Source: Moody’s

Investors tend to waive these warnings aside as they tend to think the loan to value ratios as offering adequate protection. In some ways this is true. A 60-70% loan to value ratio tends to protect the equity in most cases. At the same time some of the office sales that are occurring today are downright frightening.

The state of San Francisco’s commercial real estate market has reached a critical point, as evidenced by the significant drop in the value of the 22-storey tower at 350 California Street.

Valued at around $300 million in 2019, the building is now expected to sell for just $60 million, an 80% drop in just four years. This situation reflects the struggles faced by the city’s office real estate market, which has been severely impacted by the pandemic-induced remote work trend.

Source: The Deep Dive

If KREF had given a loan on this building at 65% loan to value, the loss would have been over $135 million.

Verdict

KREF has struggled to deliver long term value to its holders despite a very hospitable market for most of its existence.

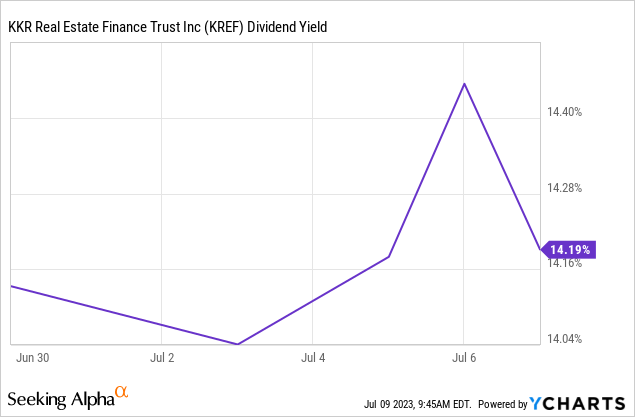

At present, the risks are high and the company will likely face some challenging refinancings over the next 3 years as its own debt comes up for renewal. While the CECL reserves look solid, we still think they will ultimately prove inadequate. That combined with the high leverage, makes us uncomfortable here, despite a very juicy yield.

For investors considering playing KREF we suggest two lower risk alternatives.

1) ACRE would be one of the lower risk plays on this sector, thanks to a leverage ratio that does not give us nausea.

2) While BXMT was a hard pass for us, BXMT bonds maturing in January 2027 are interesting. We had initially suggested those when they had a 10.832% yield to maturity. They currently yield 9.49%.

FINRA

We think both are superior to KREF common shares. We will note here that we think BXMT bonds are also better in our opinion to KKR Real Estate Finance Trust Inc. 6.5% SER A PFD (NYSE:KREF.PA) which actually yields less than BXMT debt. At present we don’t own any of these securities and think a true blow-up opportunity will arrive further down the line. In the interim we are happy picking up 7.0-7.5% yielding bonds where we see risks are non-existent.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

More Stories

Understanding the Role of Principal in Investment and Trading Strategies

Continuous Learning And Professional Development In Finance

Scaling Operations: Infrastructure And Resource Planning