Tesla (TSLA) and Affirm (NASDAQ:AFRM) are two examples of companies implementing a Zero to One vision and using first-level thinking to disrupt industries that are in inverse bubbles by breaking down the problems in their respective industries and are reconstructing the traditional business models.

An “inverse bubble” is a large, mature industry that is stagnant with little to no innovation and has a low net promoter score (NPS) while it’s worth hundreds of billions in market value. Legacy car manufacturers and legacy financial institutions are similar in many ways as they are highly fragmented industries with nearly perfect competition.

Tesla and Affirm offer 10x better products and experiences in stagnant, mature, low NPS industries; cars for Tesla, and financial services for Affirm. Both have greater missions to better society. Both are vertically integrated business models where the companies themselves are in control of their products across the entire lifecycle, from their product development and distribution to the customer experience once the product is delivered.

Introduction

Tesla and Affirm are completely different companies, but there are many parallels in how the companies are redefining their respective industries as both are uniquely vertically integrated. The claim that Affirm is the next Tesla may seem bold, but Affirm’s software-defined, data preserving, vertically-integrated payments network in many ways resembles Tesla’s electric vehicles. Tesla is defining the future of transportation when it comes to cars as it continues to set the bar for electric vehicles, full-self-driving capabilities, as well as creating a fully integrated network from charging stations, to the software inside its vehicles, to the user interface. Tesla is in a unique position to preserve data from many points of the lifecycle of its products as it learns individuals’ driving patterns to offer them tailored services, like auto insurance.

Tesla is a data preserving, vertically integrated transportation network. Affirm is a data preserving, vertically integrated payments network.

Tesla – offers a 10x better product that enables sustainable transportation of people as well as the transportation of energy through Tesla Solar

Affirm – offers a 10x better product that enables the movement of money as well as a means for people to access capital without the need to put themselves in debt every time the financial product is used for a purchase, unlike credit cards.

Tesla’s cars drive on roads, as they are the infrastructure to get you from one place to another. On the other hand, Affirm is a means for consumers to access capital while it also enables them to fund purchases immediately, where consumers are eligible for cashback rewards. Comparing Affirm to Tesla, Affirm is the car, the road is the form of money transfer (Affirm uses ACH Debit to move money), while the card networks (i.e., Visa, Mastercard, Amex) are the toll booths that allow Affirm to send money to the merchants who are a part of their networks or merchants where Affirm’s ledger is not directly integrated, as it is at Affirm’s partner merchants, like Amazon or Peloton. Affirm is the Tesla of everyday payments and everyday financial products.

Now let us explore the following four similarities between Tesla and Affirm.

A Meaningful Mission

A First Principle Vision

Visionary CEOs At The Helm

Similarities In Vertical Integration

A Meaningful Mission

Since day one, our mission has been to deliver honest financial products that improve lives. That mission hasn’t changed-and it never will.” – Affirm Mission Statement

Tesla’s mission is to accelerate the world’s transition to sustainable energy.” – Tesla’s Mission Statement

Tesla and Affirm are creating products that the world has never seen that will preserve society, whether that’s through offering delightful financial products or accelerating the world’s transition to alternative energy. Both companies are intending to do good for the future of humanity.

Below is a response from Affirm’s CEO and co-founder, Max Levchin, on the motives behind starting Affirm.

When I started looking at payments again, I realized this whole point-of-sale thing is not just an opportunity but a social ill that needs fixing. PayPal was very commercial. We knew what we were doing – we were building a product that was helping the world be more efficient in payments – but there wasn’t a huge social mission behind it. Eventually, it became a big thing and we improved a lot of people’s lives but we have a very strong point of view with Affirm. Our mission is to clean up lending because lending has a bad name for a lot of reasons.”

Affirm doesn’t charge late fees or compounding interest while making it clear what a user is subject to pay and the payment schedules when someone chooses Affirm at the checkout.

Affirm.com

Both Tesla and Affirm are pursuing missions that are important to the advancement of society which gives these companies and their leaders a social responsibility to carry out their missions.

A First Principle Vision

We can’t solve problems by using the same kind of thinking we used when we created them.” – Albert Einstein

Tesla and Affirm both implement first principle thinking when it comes to their business models and bringing their products to market as well as managing their products once they are in use. This type of thinking enables Tesla to take significant leaps when it comes to building and producing innovative products rather than making small improvements to what already exists.

I recommend watching this 2-minute interview from this link of Musk being asked about first principles thinking and how implemented at Tesla.

Clearly, Tesla’s implemented first principles thinking in its business model and this is further supported by the fact that Tesla is vertically integrated. On the other hand, Affirm has also implemented first principles thinking since its inception as Affirm controls its full-stack since the first two years of the company were spent building its stack payments system from the ground up.

One of the things that we did early on was we spent the first two years building a full-stack from scratch. So everything from the general ledger all the way to the underwriting systems is built internally. So it allowed us to be very nimble with what we want to try, how we want to build it, and how we instrument and optimize it.” – Max Levchin

Similar to how Tesla engineered its cars from the ground up with the specifications that would meet the demands of an electric engine, Affirm built its ledger and full-stack from the ground up to meet the demands of a software-defined, vertically integrated payments network. As a result, there are many similarities between Tesla and Affirm when it comes to building their products to meet the demands of problems that wouldn’t necessarily be solvable without first principles thinking.

Tesla’s self-driving electric vehicles make sense from a sustainability perspective as well as a safety perspective but Affirm’s products are also optimal for consumers. Affirm financial products are more optimal for consumers because they allow consumers to not rely on the issuance of debt each time they swipe a credit card. Affirm will offer a debit card where consumers are eligible for Cash Back rewards when they pay for purchases instantly (funded by their bank account through ACH) while they will have 24 hours to choose if they’d rather use Affirm’s BNPL products to pay for the purchase over time from the Affirm Debit + App.

Consumers with Affirm Debit + can pay for things instantly or over time from the same card which can also be stored in Apple or Android wallets. This is more optimal for consumers because they have better insights and controls to manage their cash flows, while not losing out on the rewards offered by a traditional credit card. Rather than extending a lump sum of credit for one month and allowing the consumer to build their debt each time a credit card is swiped, Affirm underwrites each transaction and extends credit based on the specific item a consumer purchases as well specific transactional and alternative data from the consumer. This enables Affirm to more effectively provide loans to worthy borrowers, rather than providing one lump sum to spend per month based on a FICO score, which doesn’t account for nearly as much data.

Affirm uses this data to understand the flow of funds between merchants and consumers. Affirm has access to SKU level data, which means it can underwrite transactions at its partnered merchants to the item-specific merchandise being purchased. This approach to credit is significantly better than just giving somebody a monthly balance based on their FICO score because each transaction is underwritten on the transaction level, something the incumbent payment networks are not capable of (I explored this topic in a separate note).” – Author’s Previous Affirm Note

Visionary CEOs At The Helm

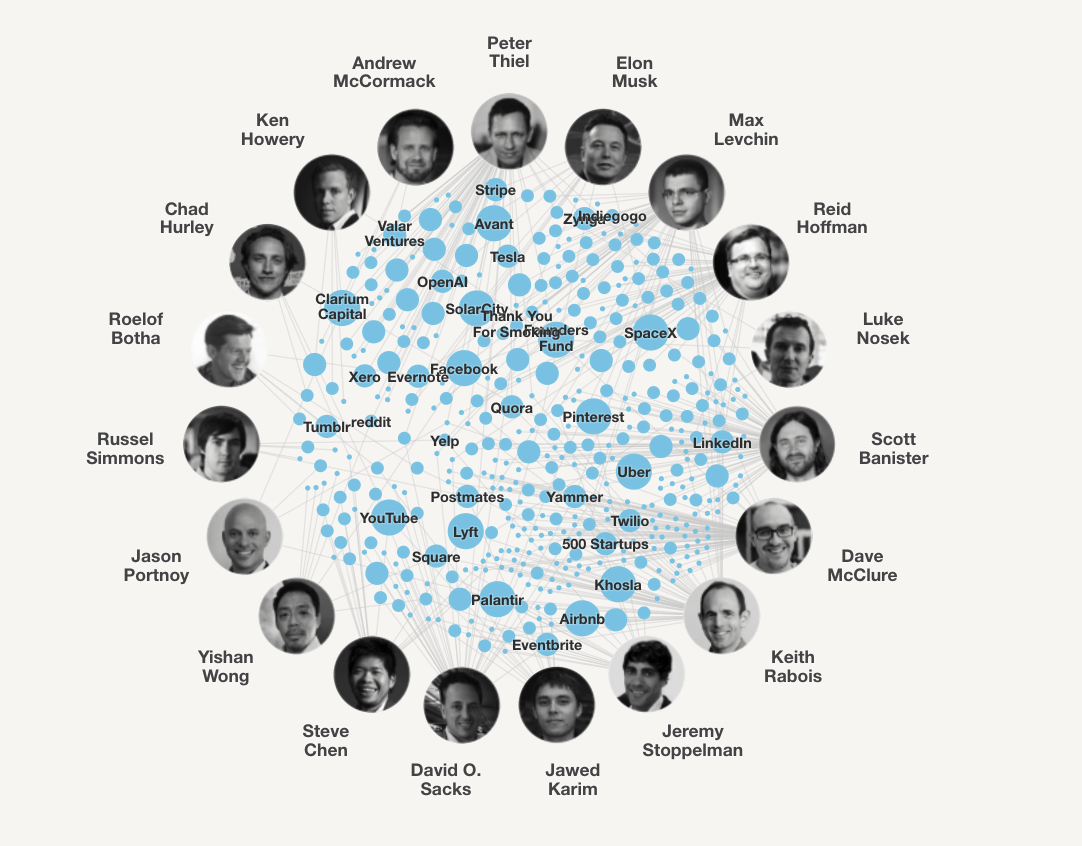

Elon Musk and Max Levchin are both well-respected thought leaders and both stem from the PayPal Mafia, the co-founders of PayPal who went on to find companies like LinkedIn, YouTube, Palantir, and Opendoor. The PayPal Mafia was an influential bunch of leaders who would go on to reshape society by building companies that would go on to pioneer industries, many of which would go on to democratize the widespread adoption of the internet.

fleximize.com

Before PayPal became PayPal, there were two companies; X.com founded by its CEO at the time, Elon Musk, and Confinity, founded by its CEO Peter Thiel and Chief Technology Officer Max Levchin, and Luke Nosek. X.com was an online, full-service bank and merged with Confinity, ultimately deciding on the name PayPal. During Levchin’s role, he was pivotal in developing the risk modeling for PayPal and the anti-fraud framework to securely send money through the internet. One of Levchin’s colleagues, Nathan Gettings, who was also Palantir’s first chief technology officer, was an engineer at PayPal where he worked closely with Levchin to fight payment fraud. The PayPal Anti-Fraud framework would go on to provide the fundamental building blocks for Palantir’s first initiative to fight counterterrorism, while Gettings and Levchin reunited in ~2011 and co-found Affirm. When it comes to fighting payment fraud, Max Levchin is king and this dates back to his days as Founder and CTO at PayPal (PYPL) when the company was losing $2,300 per hour due to fraud, and Levchin was pivotal in engineering the PayPal anti-fraud framework, which would solve PayPal’s fraud dilemma.

PayPal, never really dug below the rails, the sort of a payment industry jargon. Credit card rails is what Visa and MasterCard provide. Everything above it, is above the rails, and below the rails are the issuing banks, which actually lend the money and take the risks. People generally don’t go there, it’s very hard, you can lose 100% of the money, you can never make more than a couple of percent. So it’s a very asymmetrically distributed risk-reward thing. But if you dig deeper, you will find all kinds of yucky things like late fees that account for more than half the profits, and deferred interest which is kind of an ugly way of making money because it promises somebody a free loan, but then finds a way to charge them interest in the part that was actually supposed to be free.” – Max Levchin

Musk and Levchin are both visionary leaders who have the experience and intellectual pedigrees to meaningfully impact the world through their respective companies today, while Levchin is four years younger than his counterpart. Musk has a slew of successes and continues to make his mark on humanity through SpaceX, Tesla, and The Boring Company. Levchin went on to found Slide after PayPal, a video game company that eventually sold to Alphabet, as well as helped Square with its anti-fraud framework and underwriting capabilities. Now that Levchin’s returned to financial services, it’s his turn to reorient the payment rails and attempt to create an optimal payments network, something that wasn’t achieved at PayPal.

Similarities In Vertical Integration

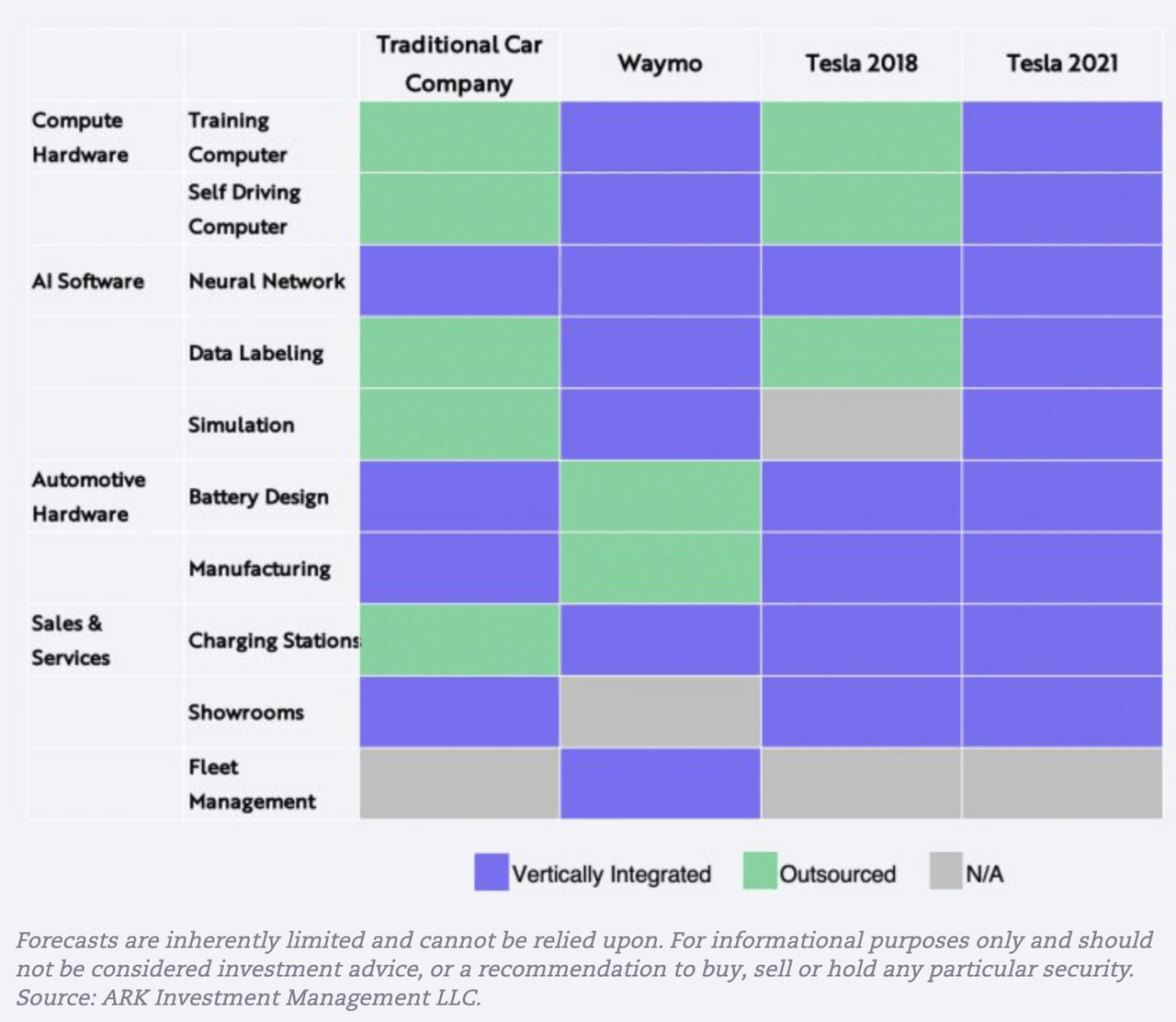

Tesla’s system is powered by AI and this is only possible because of the abundance of data that Tesla collects whether during the manufacturing process or while its vehicles are on the road. The information that Tesla collects will empower fully autonomous vehicles, but more importantly, it will allow Tesla to outsource its autonomous driving software as well as use AI to offer products such as Tesla Insurance.

Ark Invest

Tesla Insurance – Tesla is extremely vertically integrated. Tesla makes their own parts, writes its own code, as well as handles the sales for its vehicles, so there’s no better company that understands Tesla cars than Tesla itself. This is because Tesla has so many vehicles on the road today equipped with autonomous driving capabilities, specifically Tesla’s latest autopilot hardware that collects information from eight cameras and 12 ultrasonic sensors on the vehicle. It’s Tesla’s wide-vertical expansion that enables it to truly benefit from manufacturing the hardware and engineering the software to go along with it. Tesla sees that its AI will be its best asset to leverage moving forward, thanks to its growing amount of data.

Similar to how Tesla’s Autonomous Driving gets better with more data and will eventually hit full self-driving, Tesla’s insurance offering should get better as well. Tesla’s data collection is still a competitive differentiation and Tesla will need to monetize its proprietary data and AI whether that’s offering new products or services like ride-hailing or outsourcing its software to other legacy automakers. Tesla’s data will prove its greatest asset over time.” – The previous author’s Tesla Note

Affirm is similar to Tesla in the sense that it is in full control of its products, whether managing fraud, its underwriting, or directly integrating with payment networks and gateways, Affirm custom builds solutions since its ledger was built from the ground up. For example, similar to how Tesla releases software updates over the air to add new features to its vehicles as well as enhance existing ones, Affirm has the same type of capabilities with its financial products. Affirm has the same types of capabilities as Tesla when it comes to payments and offers consumers the choice of BNPL at the POS as it underwrites each consumer at the transaction level on an item-by-item basis. Affirm can also update the functionality of its virtual and physical cards over the air.

The thing that’s really cool about what we do and how we build things is this idea that we can give you a product be it a piece of plastic or an app and then update the functionality, whether it’s settlement functionality that we choose or the rewards package you’re gonna get, or the special offers you get at a retailer, we are uniquely unconstrained because we are literally updating these things on the fly, over software and we have full SKU level visibility into the data as consumers go around and transact with merchants where we are integrated.” – Max Levchin

Both Tesla and Affirm are uniquely vertically integrated, which positions both companies to capitalize on the vast amount they touch. Affirm is a payments network that preserves all of the data and information from each transaction, meaning it accumulates a lot of data from consumers, merchants, and product manufacturers, while Tesla also collects many data points from all of its cars on the road today.

Affirm is well-positioned to capitalize on the datification of the consumer credit ecosystem and open banking as it leverages artificial intelligence. Affirm will continue to vertically integrate over time, similar to how Tesla has since 2018.

Fair Value & Expected Returns

For an updated financial analysis for Affirm, I explored its latest financials and revenue growth as of its last earnings report in the note below.

Affirm: Eyes Set On Disrupting FICO

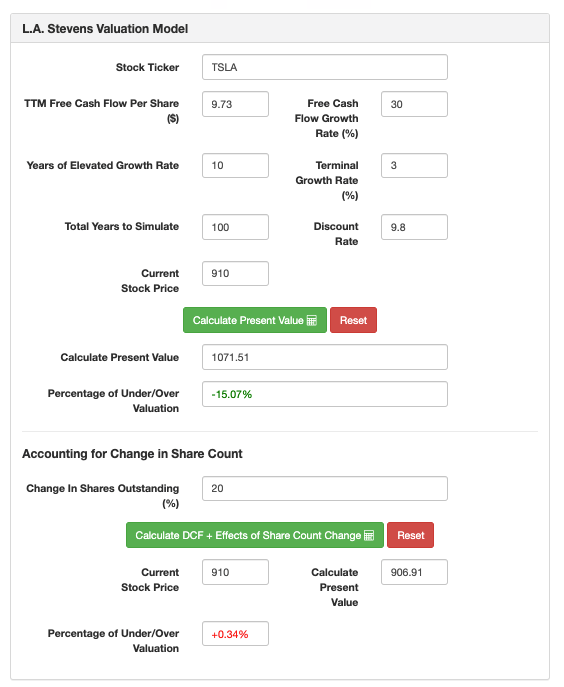

As for Tesla, the company recently reported a stellar earnings report and we’ll deploy the L.A. Stevens Valuation Model to evaluate a fair value for Tesla today. The model consists of a discounted cash flow model using free cash flow per share to assist in identifying Tesla’s value today, taking into account the change in shares outstanding. Additionally, the model uses the growth of free cash flow per share to determine Tesla’s 10-year price target, and thereby, market cap, allowing us to project Tesla’s growth over the next 10 years, which we’ll use to compare it with that of Affirm.

Assumptions:

TSLA

AFRM

Forward 12-month revenue [A]

$110B

$2.2B

Potential Free Cash Flow Margin [B]

10%

30%

Average diluted shares outstanding [C]

~1.13B

~350M

Free cash flow per share [ D = (A * B) / C ]

$9.73

$1.88

Free cash flow per share growth rate

30%

30%

Terminal growth rate

3%

3%

Years of elevated growth

10

10

Total years to stimulate

100

100

Discount Rate (Our “Next Best Alternative”)

9.8%

9.8%

L.A. Stevens Valuation Model

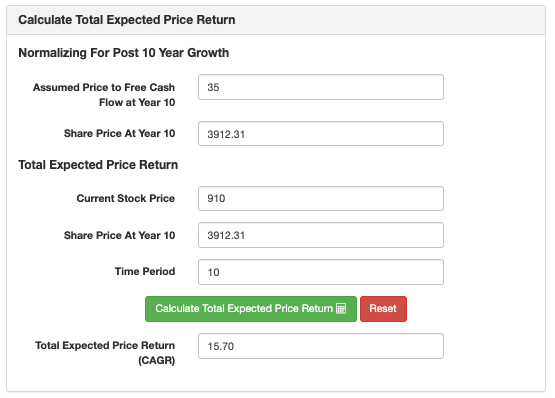

Based on our model, Tesla is trading at its intrinsic value and worth ~$907 per share. Now, we’ll use the L.A. Stevens Valuation Model to project the future value of Tesla in 10 years.

L.A. Stevens Valuation Model

Summary:

Current Price

Fair Value

Undervalued (-) or Overvalued (+)

2031 Share Price Target

Total Expected CAGR Return

Rating

Tesla

$910

$907

~0%

$3,912

15.7%

Hold

Affirm

$30

$207

-85%

$907

40%

Strong Buy

Based on conservative estimates and the results of our model, Affirm is significantly undervalued and trading at a discount compared to Tesla.

The key is paying a low price relative to something called intrinsic value. If you pay a high price relative to the value, you’re unlikely to do well and you probably have to get lucky to have a good return, but if you pay a low price relative to the intrinsic value, then the odds are on your side.” Howard Marks

Risks

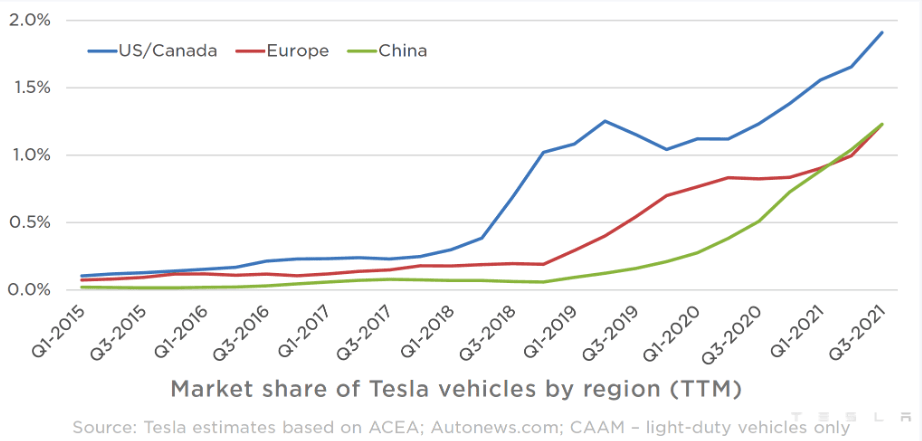

There are differences between these companies, especially given their respective industries and their goals. Tesla is clearly ahead of Affirm in its journey and this is supported by its revenue growth, profitability, and the massive mark it has made in the automotive industry thus far, as Tesla continues to gain total vehicle market share. Tesla has a 69.95% EV market share in the U.S. with the Nissan coming in second at 8.51%.

Tesla Estimates based on ACEA; Autonews.com

Tesla is gaining market share and is well on its path to generating significant growth as the demand for EVs rises over the coming decade, hence Tesla’s share price is no longer priced as if it were going bankrupt. Affirm on the other hand is only generating ~$2B in annual revenue and is still not free cash flow positive, compared to Tesla which posted ~$8.4B in net income over the trailing 12 months. Affirm’s much earlier in its lifecycle and preparing to launch a massive distribution phase to promote its financial products directly to consumers by offering everyday financial products.

Affirm first developed a solution for merchants that was 10x better than the current options at online checkout pages, but now Affirm has plans to unbundle credit cards. Affirm has plenty of work to do as it launches Debit + and attempts to capture more offline payment volume. Affirm will face competition from other large payments companies and other fintechs, but Affirm’s proprietary technology (highlighted by winning significant partnerships) ultimately makes Affirm’s payments network more appealing than the incumbents for merchants, consumers, and product manufacturers. Hence, there will be plenty of competition from other fintechs as well as incumbent financial institutions. There is also fear that a recession will negatively impact its underwriting, but management and the data support that Affirm’s underwriting is performing in line with management’s expectations. The pessimism around Affirm creates a unique opportunity for outsized returns as did Tesla for its early investors, but there are execution risks anytime investing in young growth companies. That’s why we partner with visionary leaders who operate companies with profound product-market fit; like Tesla and Affirm.

Conclusion

Tesla and Affirm are redefining their respective industries and there are many similarities between their visionary founders and execution strategies, many of which we explored. While Tesla is a great company and is well-positioned to thrive and capture more automotive vehicle market share, Tesla’s generated 1300%+ returns for investors over the past 3 years. I view Affirm today as a similar opportunity to invest in a company of this stature while its products and the fundamental premise of its business are not well understood and accepted by the media and society in general, similar to EVs.

Affirm is redefining people’s expectations when it comes to offering financial services and not feeling anxiety about hidden fees, late fees, or compound interest. I rate Affirm a conviction buy at $30, while I label Tesla a hold at its current valuation.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

")

More Stories

Understanding the Role of Principal in Investment and Trading Strategies

Continuous Learning And Professional Development In Finance

Scaling Operations: Infrastructure And Resource Planning